Quick Facts

- The Deadline: The long-standing bancassurance and wealth management partnership between Monte dei Paschi di Siena (MPS) and French insurer AXA is set to expire in 2027.

- The Strategy: Generali is aggressively pitching to replace AXA, framing the move as a matter of "Italian financial sovereignty" to keep domestic savings within the country.

- The Conflict: Generali’s bid aims to recover fee income that currently flows to France, following AXA’s sale of its asset management arm to BNP Paribas.

- The Hurdles: Success hinges on navigating a major leadership turnover at MPS scheduled for April and ongoing legal investigations into key Generali shareholders like Delfin and Caltagirone.

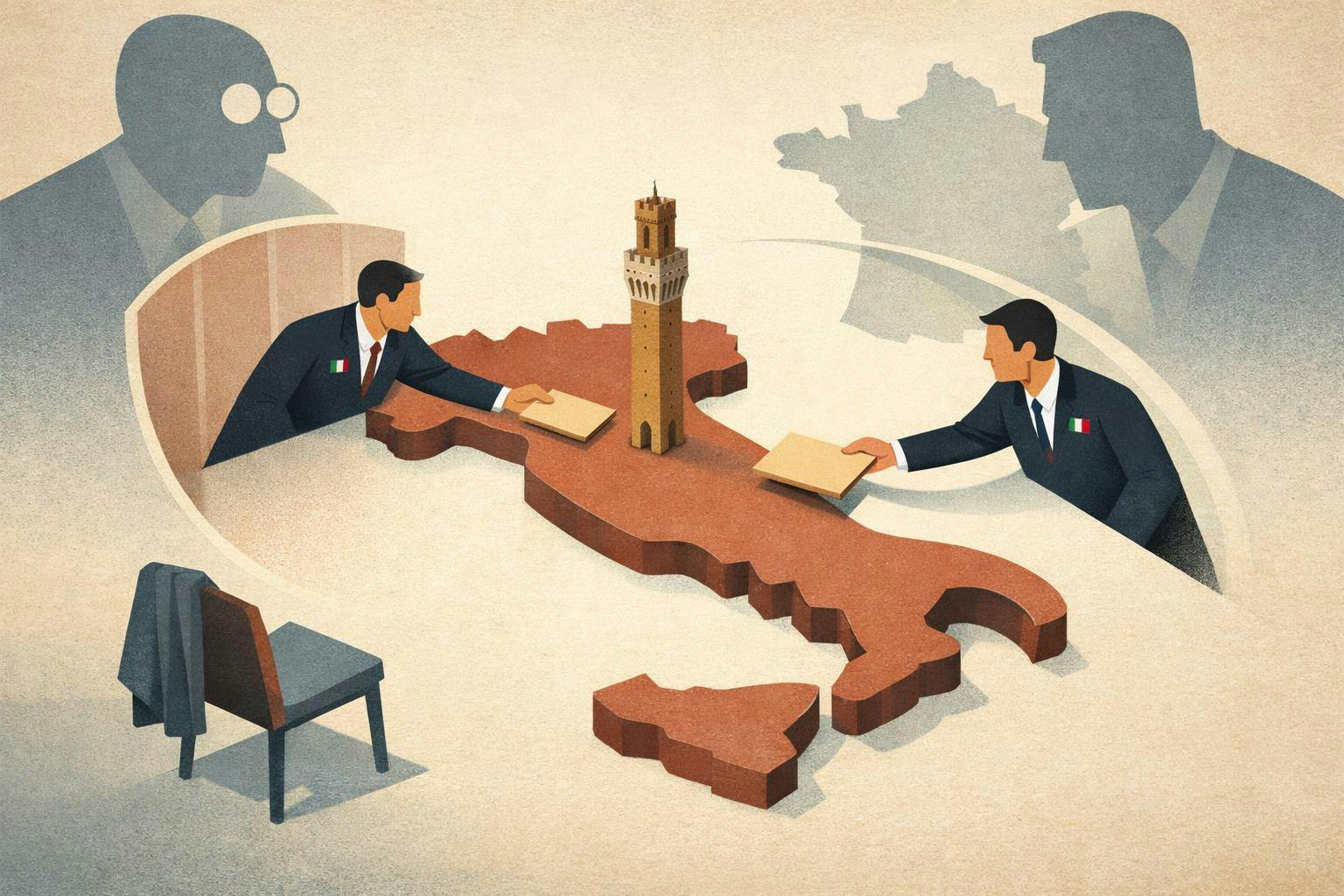

The Battle for Italian Household Savings

The world’s oldest bank, Monte dei Paschi di Siena (MPS), is at the center of a strategic tug-of-war that could redefine the Italian financial landscape. At stake is more than just a distribution contract; it is a battle for the "financial sovereignty" of Italian household savings. For decades, the partnership between MPS and the French insurance giant AXA has been a cornerstone of the bank’s wealth management strategy. However, as the 2027 expiration date looms, Italy’s champion, Generali, is making a high-stakes play to bring those assets back home.

Generali is pitching for the 2027 MPS contract to repatriate Italian household savings, which it argues are currently managed in France. This isn't just about corporate pride—it’s about the bottom line. When AXA reached an agreement to sell its asset management arm to BNP Paribas, it signaled a shift that Generali CEO Philippe Donnet viewed as an opportunity. By positioning Generali as the domestic alternative, the insurer is leaning into a narrative of national resilience, suggesting that Italian wealth should support Italian growth rather than fueling the fee engines of Parisian financial institutions.

The Challenger’s Move: Generali’s Strategic Pivot

Under the leadership of Philippe Donnet, Generali has undergone a significant transformation. The firm recently terminated its pan-European asset management venture with Natixis, a clear signal that its focus is shifting away from broad, cross-border experiments toward domestic consolidation and deeper integration within the Italian market.

This strategic pivot is fueled by a desire to capture "lost" revenue. Currently, when an MPS client buys an insurance product or invests in a fund managed under the AXA partnership, a significant portion of those management fees leaves the Italian ecosystem. Generali’s argument is simple: by switching to a domestic partner, MPS can ensure that the economic benefits of Italian wealth stay within the peninsula.

Key Financial Stats

- Solvency Ratio: Generali maintains a robust 214% solvency ratio, providing the capital cushion necessary to absorb large-scale distribution deals.

- UniCredit Stake: UniCredit currently holds a strategic minority stake of approximately 4% in Generali, signaling deep (if sometimes tense) integration within the Italian financial sector.

- Asset Shift: The termination of the Natixis partnership frees up management focus to pursue the MPS deal as a primary growth driver.

The Incumbent’s Position: Why the AXA Deal is Under Pressure

AXA has been a reliable partner for MPS, but the ground beneath that partnership has shifted. The decision by AXA to sell its investment management arm to BNP Paribas changed the optics of the deal. Suddenly, the MPS-AXA partnership wasn't just a two-way street between a bank and an insurer; it became a pipeline funneling Italian assets into the hands of one of Europe’s largest banking competitors.

The existing bancassurance and wealth management partnership between MPS and AXA is scheduled to expire in 2027, and the Italian government—which still holds a significant influence over MPS despite recent sell-downs—is increasingly sensitive to the idea of financial autonomy. For MPS, the choice is between continuing a functional, if "foreign," relationship or aligning with a domestic powerhouse that carries the flag of Italian financial sovereignty.

| Feature | Generali (The Challenger) | AXA (The Incumbent) |

|---|---|---|

| Pitch Logic | Financial Sovereignty & National Consolidation | Proven track record & European scale |

| Asset Management | Domestic-focused, integrated with Italian banks | Transitioning to BNP Paribas management |

| Political Alignment | High (Matches current "Made in Italy" sentiment) | Moderate (Standard EU corporate partnership) |

| Revenue Flow | Stays within Italian borders | Distributed to French parent/BNP Paribas |

Boardroom Chess: The Power of Shareholders and Alliances

If this were a simple business decision based on fee structures, Generali might have an easy win. But the Italian financial world is rarely that straightforward. This is a game of "boardroom chess" involving some of the most powerful figures in European finance.

At the heart of the matter is the complex relationship between Mediobanca (Generali’s largest shareholder) and a group of "rebel" investors led by Francesco Gaetano Caltagirone and the Del Vecchio family’s holding company, Delfin. These shareholders have historically sparred with CEO Philippe Donnet over the speed and direction of Generali’s growth. Their influence cannot be understated; any major move toward MPS must satisfy these heavyweights, who are often more concerned with the long-term balance of power in Milan than with short-term distribution fees.

Furthermore, the "UniCredit Factor" adds another layer of intrigue. UniCredit CEO Andrea Orcel has maintained an "observing" stance, but the bank's 4% stake in Generali makes it a silent partner in any major strategic shift. If UniCredit decides to pursue its own consolidation goals, the MPS-Generali deal could either be a catalyst or a casualty of broader banking mergers.

Major Hurdles: Leadership Turnover and Legal Uncertainty

Despite the strategic logic, the road to 2027 is fraught with obstacles. Significant hurdles for the Generali-MPS deal include the projected leadership turnover at MPS in April and legal investigations into the influence of shareholders like Delfin and Caltagirone.

Current MPS CEO Luigi Lovaglio has been credited with the bank’s remarkable turnaround, but his mandate is up for renewal in April 2025. A change in leadership at the world's oldest bank could reset the negotiation table. A new CEO might prioritize a different set of strategic alliances or perhaps seek a full merger with another bank (like BPER or Banco BPM) rather than just an insurance partnership.

Governance Risks

- Milan Prosecutors: Investigations into whether key Generali shareholders coordinated their votes illegally could paralyze decision-making at the board level.

- The April Reset: The upcoming board renewal at MPS creates a "wait-and-see" environment for all potential partners.

- Regulatory Scrutiny: Any move that looks like "national protectionism" may face pushback from European Central Bank (ECB) regulators who favor cross-border competition.

Market Context: Trends in Italian Bancassurance

The push for the MPS contract comes at a time of rapid consolidation in the Italian banking sector. As Net Interest Income (NII) is projected to decline with stabilizing interest rates, banks are becoming more reliant on fee-based income from insurance and wealth management. This makes the "bancassurance" model more valuable than ever.

We are seeing a trend toward digital wealth management and the integration of ESG (Environmental, Social, and Governance) factors into insurance products. Generali is betting that its local knowledge will allow it to tailor these products more effectively for the Italian demographic than a French-owned entity could. If Generali wins, it won't just be taking over a contract; it will be setting the template for how Italian banks and insurers can defend their home turf against the encroachment of pan-European giants.

The Verdict for 2027

Will Generali win the MPS contract? The strategic momentum is certainly on their side. The narrative of "financial sovereignty" is powerful, especially in the current political climate, and AXA's transition to a BNP Paribas-led asset management model has created a clear opening.

However, from a risk-aware investor perspective, the "boardroom chess" remains the wildcard. The outcome depends less on the merits of the insurance products and more on the resolution of shareholder disputes in Milan and the selection of the new MPS leadership in 2025. For long-term investors, the move signals Generali's commitment to its domestic core, but the journey to the 2027 finish line will be anything but a straight path.

FAQ

Why is the 2027 date so important? The year 2027 marks the end of the current exclusive distribution agreement between MPS and AXA. Negotiations for the next cycle usually begin 18–24 months in advance, making 2025 the critical year for decision-making.

How does the AXA/BNP Paribas deal affect Italian savers? Technically, the quality of management may remain high, but the "repatriation" argument suggests that keeping management fees within Italy allows that capital to be reinvested in the domestic economy, supporting Italian sovereign debt and corporate growth.

What role does the Italian government play? The Italian Treasury still holds a significant stake in MPS. While they are committed to privatizing the bank, they have a vested interest in ensuring that MPS remains a stable, profitable pillar of the Italian financial system, which aligns with Generali’s domestic-first pitch.